Shriram Properties Limited is tapping the capital markets with its fresh issue for Rs 250 crs and an offer for sale of Rs 350 crs. The issue opened on Wednesday the 8th of December and closes on Friday the 10th of December. The price band is Rs 113-118.

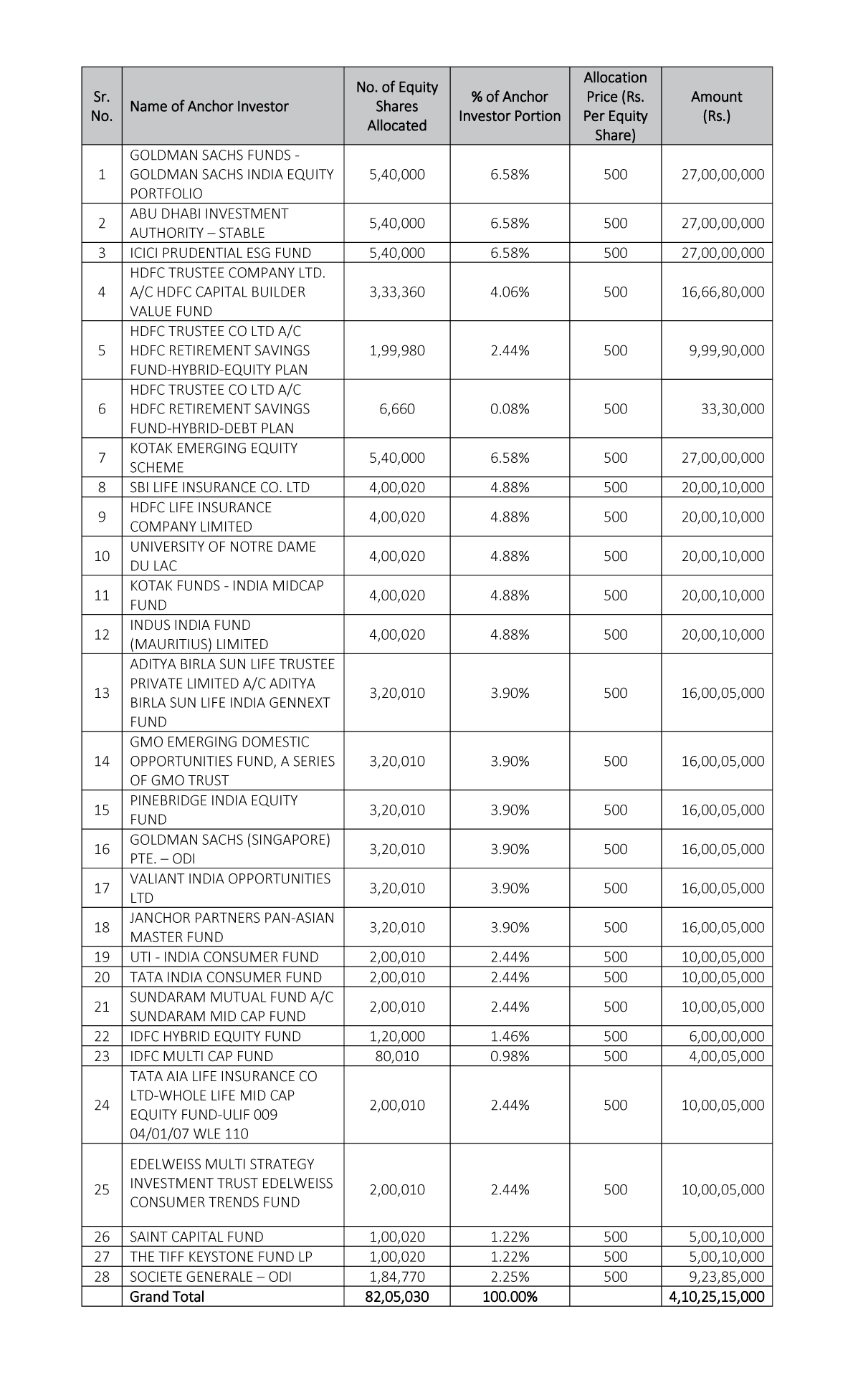

The company has completed allocation to anchor investors where it allotted 2,27,66,949 shares at Rs 118 which at the top end of the band to 10 anchor investors comprising 30 entities. The highest allocation was made to Nomura who was allotted 42,37,375 equity shares or 18.61% of the anchor book. This was followed by SBI Life Insurance who was allotted 37,29,000 shares or 16.38% of the anchor book. Nippon Mutual fund was allotted 33,89,875 equity shares or 14.89% of the anchor book. Sundaram Mutual Fund was allotted 11.14% of the anchor book.

Domestic mutual funds were allotted 84,74,625 equity shares or 37.22% of the anchor book. The top 4 anchors were allotted 61.02% of the anchor book. The anchor is encouraging and gives comfort to investors looking to invest for the medium to long term.

The company is one of the leading residential real estate developers in South India with a focus on the affordable and mid-market segment. Over the last nine years, the company is amongst the top five companies in terms of a number of units launched in Chennai, Bengaluru, and Hyderabad. The company also has its presence in the mid-market premium and luxury segments.

Its business model is an asset-light model where it does not own land but executes under JV (joint venture), JDA (Joint development agreement), and DM (development management). Except for a large land parcel in Kolkata which the company had acquired through an auction, it has no land parcels anywhere in the country. Even the one in Kolkata was acquired way back in 2008 and possession were taken in 2010. As of date, it has completed 17 msf (million square feet) through 29 projects. It has currently 47 msf through 35 projects and has land reserves to develop 21 msf in Kolkata.

The 47 msf of projects which are under development are well diversified in terms of geography with 23.2 msf in Bengaluru, 10.3 msf in Kolkata, 8.20 msf in Chennai, and 5 msf others. In terms of segment focus of this 47msf, an equal 16.7 msf is in the affordable and mid-market segment while the balance 13.3 is others. The company is well poised to deliver and hand over flats of over 3 msf of equivalent every year over the next three years at the bare minimum. This would ensure a significant rise in revenues and also ensure that the company reports profits at the net level. A key element of Shriram Properties is the fact that they are able to sell a significant 1/3rd of the area at the launch of a new project. This helps in maintaining a steady cash flow for the concerned project as well.

The company has marquee investors which include Walton, Tata Capital, and TPG at the company level and many other names in individual project level partnerships. The PE investors own 58% of the company as a whole. The group brand ‘Shriram’ has 40 plus years of operating history in India. It may be mentioned at this point that even such a strong brand has had its share of failures. Two group companies that had tapped the markets in the period 2008-2012 have not done well at all and have been a sore point with the investing public. This notwithstanding the flagship company, Shriram Transport and Finance is an icon in itself.

Post covid-19 real estate has seen a strong demand revival. While property prices may not have increased in any significant manner, the demand increase has ensured that builders across the length and breadth of the country have seen a surge in demand and liquidation of any unsold inventory. Shriram Properties in any case did not have any unsold inventory of ready flats or homes.

The company has reported losses in the last two years and the first half of FY22 primarily because of disruption of covid-19 and a result of accounting standards which stipulate that institutional investment is shown as debt and account for interest costs on structured investments. As a result of the losses, there are no EPS and hence no PE. There is another matrix by which real estate companies are valued and that is the discounted cash flows from ongoing projects adjusted for debt. Shriram Properties had filed its DRHP in 2019 earlier and had at that time in the various papers submitted, shown this value to be in the region of Rs 3200-3500 crs. The current value of the company at the top end of the price band of Rs 118 would be at a steep discount to this value.

Considering that the fresh issue is for Rs 250 crs this would unlock substantial value for investors looking to make decent returns in the short to medium term as well. Long-term investors would stand to gain substantially more.

Apply for the issue for decent gains which would also be at the time of listing.