Markets were in a festive mood with Diwali around. It was a different thing that the ‘Muhurat” trading did not oblige where markets fell in the special short one-hour session on global cues. This led to markets closing in the negative for the week albeit small losses.

The week ahead sees October futures expire on Thursday the 26th of October and currently bulls have a upper hand with the series higher by 377.60 points or 3.72%. This time Thursday would be extremely volatile and would throw up trading opportunities intraday.

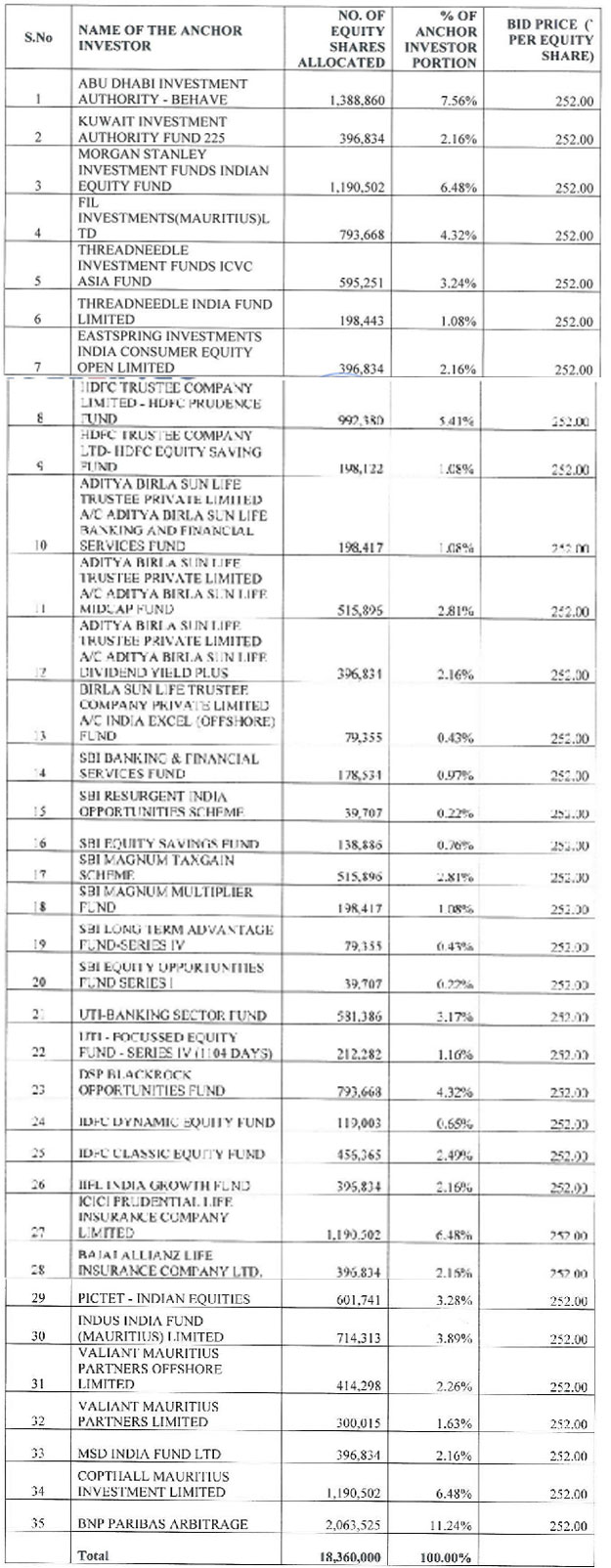

The primary market juggernaut continues to roll in a manner which is characteristic of leading to a precipice. We have two listings, one issue open for subscription and a minimum of three issues having their roadshows during the week. Shares of IEX Limited and GIC RE (General Insurance Company Limited) would be listing in the first half of the week. The only issue to be opening this week would be the one from Reliance Nippon Life Asset Management Limited would be raising between Rs 1511.64 crs to 1542.24 crs through 6.12 cr shares in a price band of Rs 247-252. This would be the first AMC or asset management company to list in India. There would be roadshows from New India Insurance, Khadims and Mahindra Logistics.

During the last week we had two listings. Shares of Godrej Agrovet listed and recorded gains of over 28% at weekend, while those of MAS Financial Services Limited gained 43%. The kind of liquidity which is available with NBFC’s and they deploying in the primary market through funding of HNI applications has assumed dangerous proportions. A company looking to raise Rs 500 to 1000 crs garners HNI funding support of between Rs 40,000 to Rs 60,000 crs and makes the entire ecosystem filled with fraught. This fraught could be extremely dangerous when things turn over and instead of listing gains we have losses.

Take the recent case of the listing of MAS Financial Services Limited which was issued at Rs 459 and oversubscribed 378.53 times by HNI’s. The cost of funding was Rs 183. The average traded price of the day was Rs 657 and hence on an application of for Rs 100 crs, he made a profit of Rs 86,073. This was because the gains made by the share on day one was over 42%. Now for a moment assume the share listed with gains of only 30% this profit would turn into a loss of Rs 2,62,435. A gain of 30% on listing day is also an excellent return and the merchant bankers would face flak for under-pricing but their HNI friends would be cursing them as they lost money. It would be a good point to debate whether the high valuations at which IPO’s are coming these days in the region of 45-50 PE multiple is anything to do with this leverage system.

There would be some big results in the week including those from Hindustan Unilever, Infosys, HDFC Bank, ICICI Prudential and Glaxo Pharmaceuticals. These results coming from different sectors would give a bird’s eye view of how the economy is faring. Last week we saw private banks coming under fire after Axis Bank declared a poor set of numbers on deteriorating asset quality and the share lost 15.4%.

Markets would be different when December begins as there would be conviction in them about the state of corporate earnings. Whether the elusive growth is intact or still a few quarters away would be public knowledge in the next 7-10 days. Keep your fingers crossed and hope for the best.