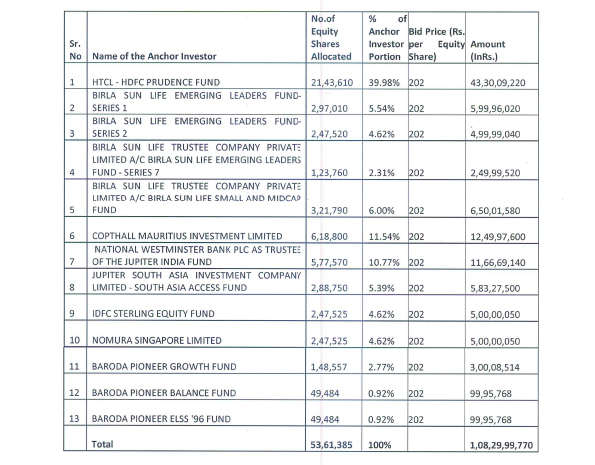

HPL Electric & Power Limited (HPL) is tapping the capital markets with its fresh issue for Rs 361 crs in a price band of Rs 175-202, completed its allocation to anchor investors. A total 53,61,385 equity shares were allotted to 9 anchor investors comprising of 13 entities at Rs 202. The largest allocation has been made to HTCL – HDFC Prudence Fund of 21,43,610 shares or 39.98% of the anchor allotment.

The issue has opened today Thursday the 22nd of September and closes on Monday the 26th of September. The full list of anchors and their allocation is appended below: –

HPL Electric & Power Limited – Completes allocation to Anchor Investors

September 22nd, 2016

Comments Off on HPL Electric & Power Limited – Completes allocation to Anchor Investors

ICICI Prudential Life Insurance Company Limited – Issue Subscribed

September 22nd, 2016

Comments Off on ICICI Prudential Life Insurance Company Limited – Issue Subscribed

The offer for sale from ICICI Prudential Life Insurance Company Limited (ICICI Pru) was oversubscribed. The company had through an offer for sale launched its IPO for 18.13 cr shares in a price band of Rs 300 to 334. The company had earlier allotted 4.89 cr shares to 38 anchor investors comprising of 69 entities at the top end of the price band at Rs 334.

The issue which included a reservation of 10% for shareholders of ICICI Bank was overall subscribed 10.48 times. At this level the total amount of funds garnered was Rs 58,240 crs, which is 1.2 times the market cap of the company going public at the top end of the issue price. The market cap of ICICI PRu would be Rs 47,940 crs at Rs 334.

This company has created a new record in the number of applications received. A total of 11.7 lakh applications were received beating the record of 11.19 lakh applications received by MAhanagar Gas Limited. The registered investor base has reached out to this issue and it has garnered the maximum possible across categories, particularly retail. The number of 1.42 times subscribed in retail should be viewed from the fact that the issue has garnered 11.7 lakh applications and the sheer size of issue at Rs 5,400 crs (minus shareholders reservation) or Rs 1,890 crs is huge by all standards.

The full details of the subscription bucket wise is given below: –

| Category | Bucket Size | Shares Applied for | Times oversubscribed |

| QIB | 32641391 | 386211540 | 11.83 |

| HNI | 24481043 | 698985584 | 28.55 |

| Retail | 57122434 | 81213572 | 1.42 |

| Shareholders | 18134105 | 221290652 | 12.20 |

| Total | 132378973 | 1387701348 | 10.48 |

From the table above it can be seen that the large oversubscription in shareholders category is partly from leveraged applications made by HNI’s here as well. There effective funding cost per share is lower here than what it would be in the HNI category. The cost of funding at around 4.5% is Rs 8.25. The grey market premium is in the region of Rs 10-11. Important news for retail investors is that all those who have applied for one or two lots would get firm allotment considering the data that is available.

Retail investors are back and have applied in their highest number ever.

ICICI Prudential Life Insurance Company Limited –Great business opportunity

September 21st, 2016

Comments Off on ICICI Prudential Life Insurance Company Limited –Great business opportunity

ICICI Prudential Life Insurance Company Limited (ICICI Pru) which is tapping the capital markets with its offer for sale of 18.13 cr shares in a price band of Rs 300-334 is more than halfway subscribed. The issue had opened on Monday the 19th of September and closes on Wednesday the 21st of September. The company had earlier allotted 4.89 cr shares to 38 anchor investors comprising of 69 entities. The allocation was made at the top end of the price band.

There is a reservation of 10% of the total issue for shareholders of ICICI Bank. The company is in the insurance sector and offers investment and protection products. It is one of the largest private players in the space and has a higher than double digit (11.3%) market share in a business which continues to be dominated by state run LIC with a 50% market share. It has a field force of over 1.21 lac agents and the product is sold by over 4,500 branches of ICICI Bank and Standard Chartered Bank.

The parentage of ICICI Prudential is marquee with ICICI Bank owning 67.6% pre-IPO and Prudential owning 25.87%. The IPO is an offer for sale from ICICI Bank and there holding would reduce by the size of offer.

The company is highly profitable and earned a net profit of Rs 1,653 crs. The designated dividend from the company is 40% but they have been paying much higher and paid a total of 84% dividend for the financial year. The amount higher than the board policy is by way of special dividend.

The area of concern that investors have is multiple of embedded value at which the shares are being offered. Last year end in December 2015 there was an issue to investors including Azim Premji who invested at an embedded value of 2.4 times. Earlier in July August 2016, the merger of HDFC insurance business with Max insurance was done at an effective embedded value of 4.3 times. The situation post liberalisation of the insurance sector has changed dynamics of this business.

The JDY or Jan Dhan Yojna and the subsequent insurance scheme thereafter saw over 3 cr new people being insured. This virtually doubled the base of people who had some protection. With such an under penetrated market it would continue to grow at 30 and 40% for the next few years. It is this growth potential and opportunity which gives the higher multiple to embedded value.

I believe the offering may look expensive but offers scope for growth and appreciation in the medium to long term. This stock is not for the listing gain player or the short term player. Apply if you have conviction in the India story.

At the end of day two, the issue is subscribed 0.52 times with QIB portion 0.59, HNI 0.15, Retail 0.65 and Shareholder 0.48. There were a total of 5.07 lakh applications received. The numbers will be on an upswing as QIB’s, HNI’s and Shareholder categories bidding ends at 4pm while retail bidding continues.

SEBI Disclaimer: – I have applied in the issue.